Charitable Contributions Subject To 10 Floor

March 2019 Charitable Contributions Are They Still Tax Deductible Marin Financial Advisors

The Charitable Contributions Deduction Mercatus Center

The Tax Break Down Charitable Deduction Committee For A Responsible Federal Budget

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

Covid 19 And Charitable Contributions By Individuals And Businesses The Cpa Journal

Https Fas Org Sgp Crs Misc If11022 Pdf

Multiply line 11 by 0 6.

Charitable contributions subject to 10 floor. Subtract line 13 from line 10. Special rule for california wildfire relief contributions. Qualifying charitable contributions made between october 8 2017 and december 31 2018 to california. Temporary suspension of limits on charitable contributions in most cases the amount of charitable cash contributions taxpayers can deduct on schedule a as an itemized deduction is limited to a percentage usually 60 percent of the taxpayer s adjusted gross income agi.

The cares act allows individuals who do not elect to itemize their deductions to take up to a 300 above the line deduction in arriving at. Cash contributions subject to the limit based on 60 of agi if line 10 is zero enter 0 on lines 12 through 14 12. Subtract line 13 from line 10. The cares act increase these amounts to 25 of taxable income for 2020.

The charitable deduction limitation for cash contributions to certain public charities and private foundations is increased to 60 from 50 of an individual s agi for the year. Casualty loss before 10 limitation after 100 floor. One of the major deviations that sets trusts apart from individuals is the applicability of deductions for charitable contributions. Not in a federally declared disaster area 19 000.

Enter the smaller of line 10 or line 12 13 14. Unreimbursed employee expenses subject to the 2 of agi limitation. 14 noncash contributions subject to the limit based on 50 of agi. Enter the smaller of line 10 or line 12.

Allowance of partial above the line charitable contributions. Qualified contributions are not subject to this limitation. Trusts have the same limitations for investment interest expenses can take real estate tax deductions and have separate deductible items subject to the 2 floor. Cash contributions subject to the limit based on 60 of agi if line 10 is zero enter 0 on lines 12 through 14 12.

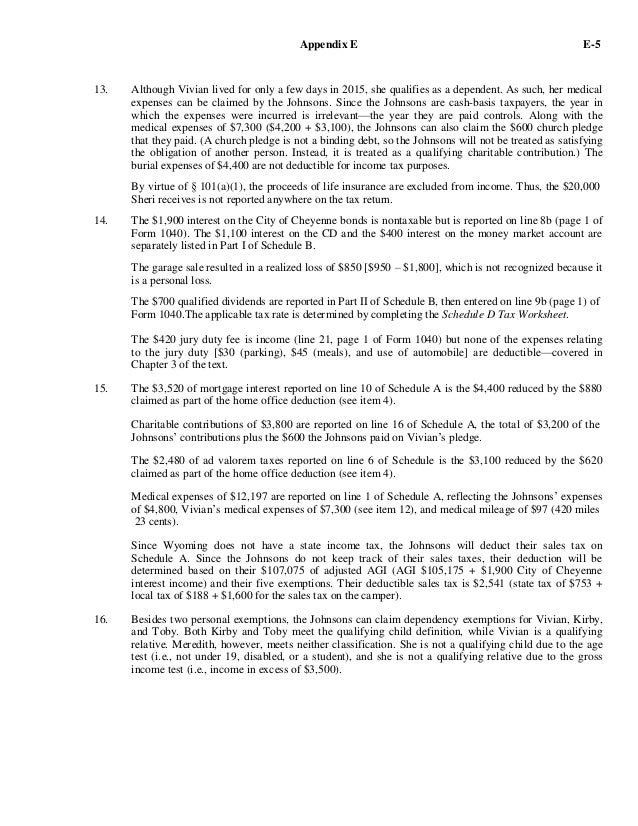

Charitable giving paper message on assorted cash. 14 noncash contributions subject to the limit based on 50 of agi. The 100 of agi contribution limit applies only to gifts of cash directly to charities not including family funded private foundations. Donations in excess of 25 may be deducted in the following five years.

Pin By Morgan Jackson On Procurement And Sponsorship Lake Oconee Charitable Donations Public Service

Acceptance Package College Acceptance Acceptance College

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Wsj Tax Guide 2019 Charitable Donation Deduction Wsj

Typically Building A House Takes Months Yet A San Franciso Based Company Managed To Build One In Just 24 Hours Located In 3d Printed House 3d Printing House

Prepping Consigned Items For The Sales Floor Flooring Sale Resale Shops Sale

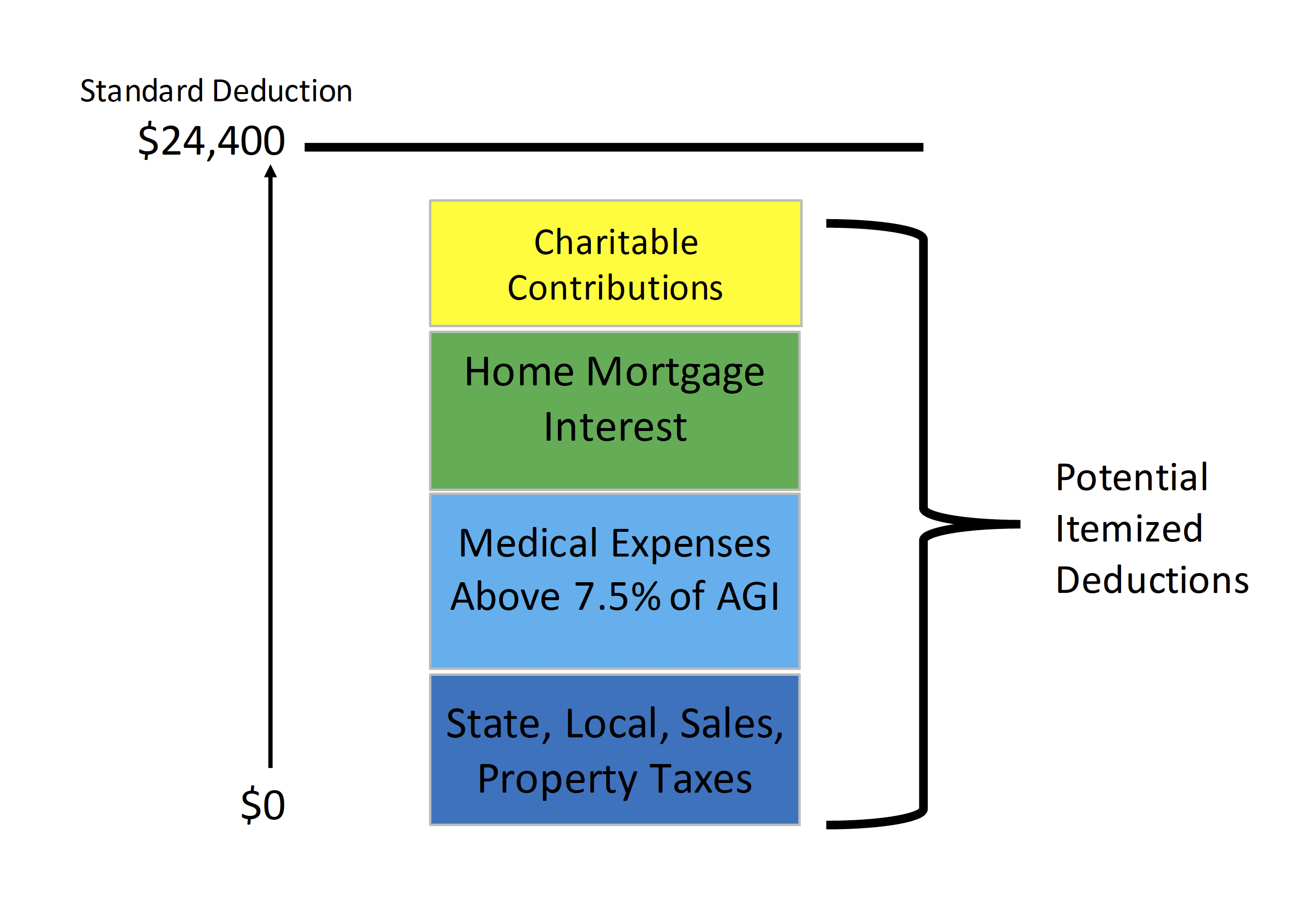

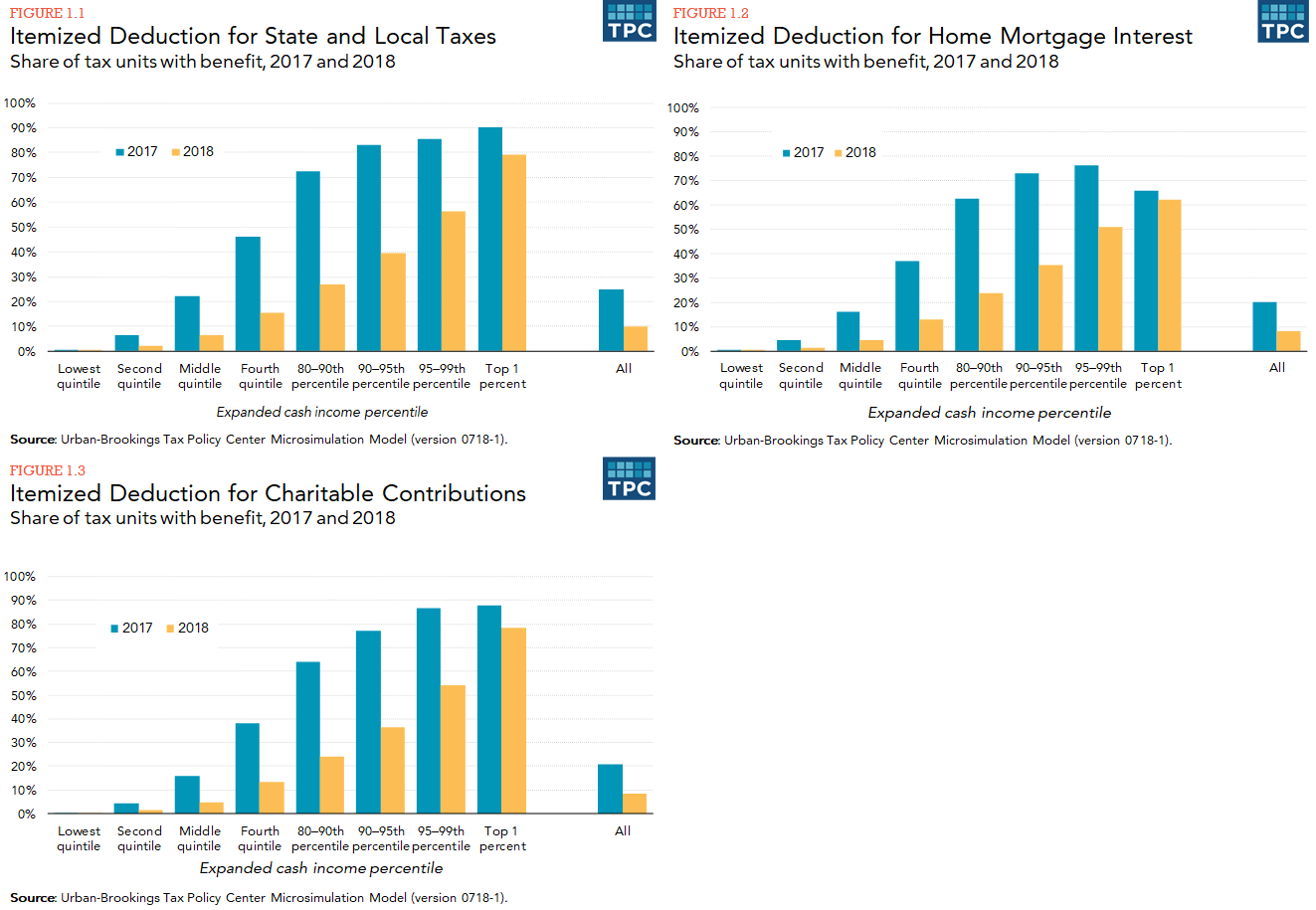

How Did The Tcja Change The Standard Deduction And Itemized Deductions Tax Policy Center

Cares Act Summary Of Tax Provision Blogs Coronavirus Resource Center Back To Business Foley Lardner Llp

43 Ideas Office Decor For Cubicle Professional Must Popular 2019 In 2020 Home Improvement Projects Home Improvement Home Business

10 Most Charitable Celebrities From The 2012 Oscar Nominees Paris Movie Paris Poster Movies

Eastern Connecticut State University Offers A Variety Of Intramural Sports To Participate In The Intramural Sport Intramurals Softball League Women Volleyball

Thompson S Transformation Grid Analysis For The Transition From The Eocene Hyracotherium Skull Form A To The Mo With Images Linear Interpolation Paleontology Mathematics

Funeral Etiquette Funeral Planning Funeral Etiquette Funeral Checklist

Not Every Charitable Donation Is Tax Deductible Gordon Fischer Law Firm

Sanitizing Footbath Floor Mat 24 In 2020 Flooring Floor Mats Cool Inventions

15 Crazy Places For Logos At Events Bizbash Event Event Ideas Creative Corporate Events

Ken Taylor Cheerwine Avett Brothers

Donating Real Estate To Charity What To Know Bader Martin

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctyqeirbje Qet1or2nq Atawapv Ahcg0s7mkn1eolrxxxs434 Usqp Cau

Https Www Jct Gov Publications Html Func Startdown Id 4506

Subtraction Tricks Teaching Math Math Classroom Homeschool Math

Leaping Forward The What And Why Of Edge Computing Edge Computing Is Proving Itself To Be A Durable Conversation Starter Among A Particular Set So It S

Plastolux Keep It Modern Commercial Design Design Workplace Design

Volunteer Thank You Letter Samples Unique Volunteer Appreciation Letter Sample In 2020 Reference Letter Appreciation Letter Reference Letter Template

2019 Tax Planning Guidelines For Individuals And Businesses The Ledger Mazars Usa The Ledger Mazars Usa

Pin On Irfan

Charitable Giving Increased In 2019 Study Thehill

Check Out New Work On My Behance Portfolio Business Plan Essentials Http Be Net Gallery 38806373 Busines Business Planning How To Plan Best Business Plan

How Much In Charitable Deductions Can I Claim Before I M Red Flagged

Italian Villas On The Maine Coast Eegonos Vintage House Plans Maine Coast Italian Villa

Did Nfl Player Just Defy Gravity Nfl Players Sports Memorabilia Soccer Field

Eventfully Angela A Football Themed 40th Birthday Party 40th Birthday 40th Birthday Parties Football Birthday

The Tape Treats The Entire Roll Of Sticky Film As A Canvas For Useful Information Made From Vinyl The Tape Comes With L In 2020 Tape Hex Bolt Magnetic Tape

Myhr Charitable Giving

9 11 Cafe Concept Store Wip On Behance Cafe Concept Concept Store Wayfinding

Oratory Of St Joseph Congregation Of Holy Cross Oratory Holy Cross Saint Joseph Montreal

Lgbtq Rainbow Dipper Dipper Vaporizer Rainbow

The Empty Bowls Project Bowl Ceramics Projects Projects

Chapter 2 Corporations Introduction Operating Rules Ppt Video Online Download

Installation Galleries Artesanato Projetos

Solutions Manual For South Western Federal Taxation 2017 Comprehensiv

5 Things Not To Say In Grant Applications Grant Application Grant Writing Business Grants

Acct 3220 Taxation Midterm Ch2 Flashcards Quizlet